Teladoc, Livongo, and The Promise of Digital Health (Part 1)

Teladoc, Livongo, and The Promise of Digital Health (Part 1)

Can the blockbuster deal accelerate the evolution of healthcare from reactive, episodic, and on-site to value-based care that is proactive, continuous, and remote?

Digital health witnessed its biggest acquisition in history last week.

From Forbes, August 07, 2020,

Teladoc and Livongo recently announced their merger, bringing together two digital health powerhouses. This is the largest digital health deal in history, ringing in at a purchase price for Livongo at $18.5B, and creating a combined entity worth $38 billion. This deal eclipses Amazon’s acquisition of PillPack and Google’s $2.1 billion bid for FitBit.

Why is this transformative and what does it mean?

To unpack, it is critical to understand: 1) The state of healthcare spend in the US, 2) The history and role of employers in the US healthcare system, 3) The rise of pro-active and continuous engagement solutions to manage chronic conditions, and 4) The meteoric growth of remote virtual care, now accelerated by COVID. I will discuss in Section 5, my thoughts on the deal, and its implications for the future of the digital health ecosystem.

#1: State of US Healthcare Spend

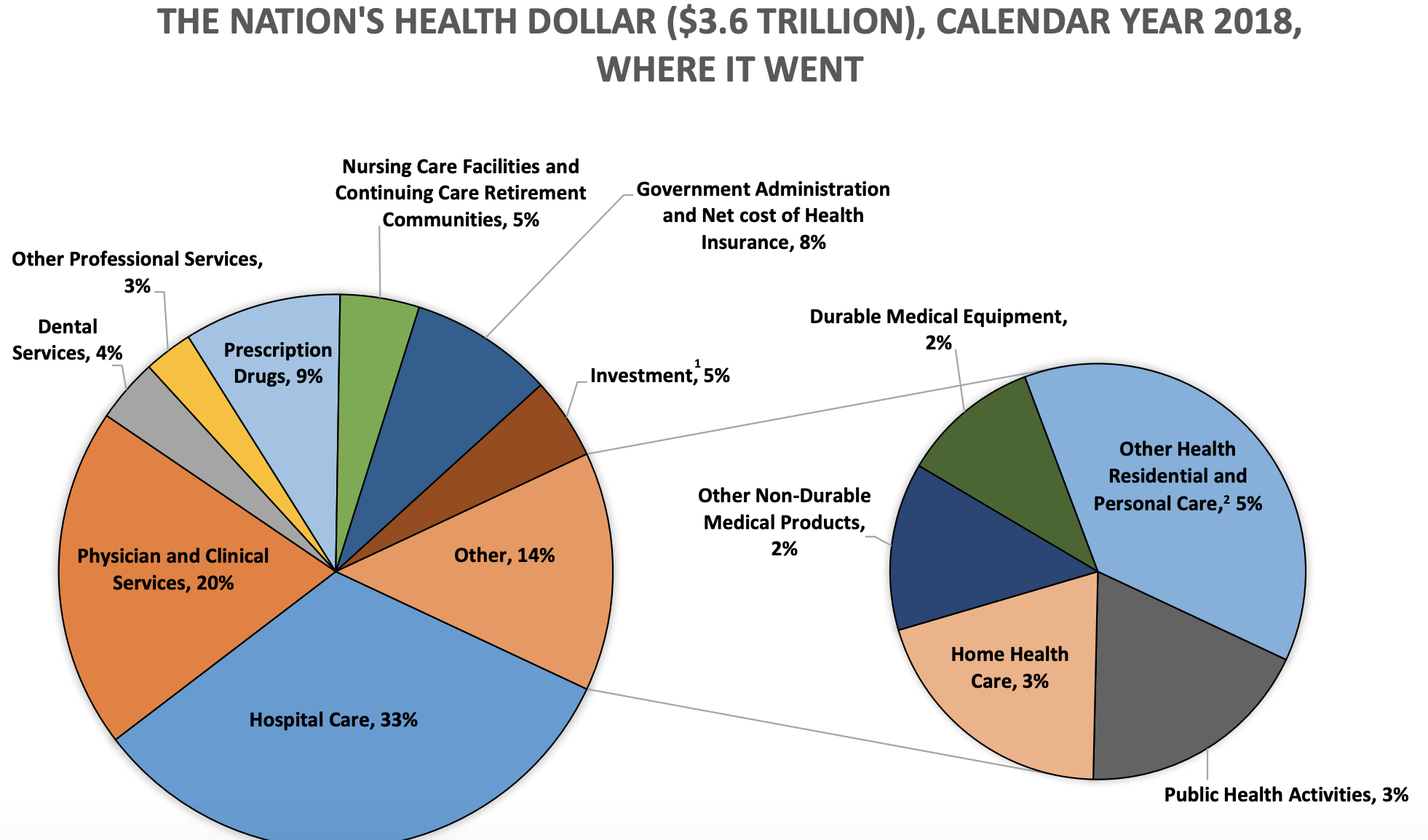

The US has the highest per capita spend among nations: $11,172 per person and a total spend of >$3.6 trillion (2019).

According to the CDC, 75-90% of this $3.6 T spend is towards chronic diseases [1]

In terms of public insurance, treatment of chronic diseases constitutes an even larger proportion of spending - 96 cents per dollar for Medicare and 83 cents per dollar for Medicaid.

A report by the Milken Institute lays out this data in more detail.

When the indirect costs of lost economic productivity are included, the total costs of chronic diseases in the U.S. increase to $3.7 trillion, almost 19% of GDP.

The US spends substantially more on healthcare spend per capita, but has significantly worse health outcomes. Our healthcare system is better described as “sick care” that is periodically activated by “episodes” that bring the patient to the hospital to generate revenue for payers, providers, brokers, and drug makers. Current models do not substantively address underlying behavioral factors, or support proactive and continuous management of risks related to chronic conditions.

The business of healthcare has been more successful in the US than the practice of healthcare. Or to put it bluntly, the healthcare eco-system optimizes for payers and providers making money, not patients’ long term success.

Nevertheless, at 18% of GDP, Healthcare is the country’s largest industry. Providers —Health systems, Hospitals, and Clinics —are reimbursed by both public payers (Medicare, Medicaid) (~ $840 B) and large private insurance firms (~$1T) like United, Humana, Aetna, and Anthem; Almost all of the $1T paid out by private payers is funded by employers who pay sky-high premiums to sustain the value chain.

Despite the best efforts of the Affordable Care Act, questions of access, cost, and quality still plague the system.

New technologies and increased public awareness are cause for hope and change. But can it drive a fundamental shift in the operating model? To understand more, it is important to take a closer look at the role of the employer.

#2: The Employer and US Healthcare

In 1940, only 9 percent of Americans had some form of health insurance. This was typically offered by groups of physicians or hospitals, not employers. Few people wanted insurance.

But things changed during World War II.By 1950, more than 50 percent did. By 1960, more than two-thirds did.

How did this happen?

To paraphrase from this NY Time op-ed in 2017,

“In 1942, with so many eligible workers diverted to military service, the nation was facing a severe labor shortage. Economists feared that businesses would keep raising salaries to compete for workers, and that inflation would spiral out of control. To prevent this, President Roosevelt froze wages. Businesses were not allowed to raise pay to attract workers.

Businesses were smart, though, and instead they began to use benefits to compete. Specifically, to offer more, and more generous, health care insurance.

Then, in 1943, the Internal Revenue Service decided that employer-based health insurance should be exempt from taxation. This made it cheaper to get health insurance through a job than by other means.

After World War II, Europe was devastated. As countries began to regroup and decide how they might provide health care to their citizens, often government was the only entity capable of doing so, with businesses and economies in ruin. The United States was in a completely different situation. Its economy was booming, and industry was more than happy to provide health care.”

One of the unintended but not surprising consequences of employer-offered insurance is that wages have stayed stagnant over decades while employer-paid premiums keep rising at ~ 5% per year. There is indeed evidence that employer sponsored insurance is hurting Americans’ paychecks.

Premiums have risen so much that the total cost for employer-provided health coverage for a family plan passed $20,000 in 2019.

From the Wall street Journal on Sept 25, 2019 (slightly edited for clarity).

“$20k is a milestone,” said Drew Altman, chief executive of the Kaiser foundation. “It’s the cost of buying an economy car, just buying it every year for every employee.”

As a point of comparison, Corporate taxes as a % of GDP has declined over the last 50 years from 4% to 2% while healthcare has ballooned from 5% to 17+%.

And Corporate America pays the biggest chunk of these rising healthcare costs. “Every Large Employer is a Health Pan,” Warren Buffet said in 2019, pointing out that addressing the tapeworm of healthcare costs should be the top priority of every CEO.

Providers are often accused of driving up healthcare costs, with appropriateness of care and price gouging being the two most rampant concerns. Payers swimming in huge profits find it easier to increase employer premiums every year than fix the messy “markup and discount” games providers and payers play. That leaves the employer as the only party most incentivized to reduce costs for the right reasons: Healthy employees are happier, enjoy higher productivity, incur lower healthcare costs, and churn less.

Thus the self-funded or the fully insured employer has emerged as the primary buyer, influencer, and catalyst for digital health solutions that drive pro-active detection and ongoing monitoring.

In Part 2, I will discuss the emergence of chronic management solutions, virtual care, and the rationale and implications of the merger.