The Origins of Our Discontents - Part 2

The Origins of Our Discontents - Part 2

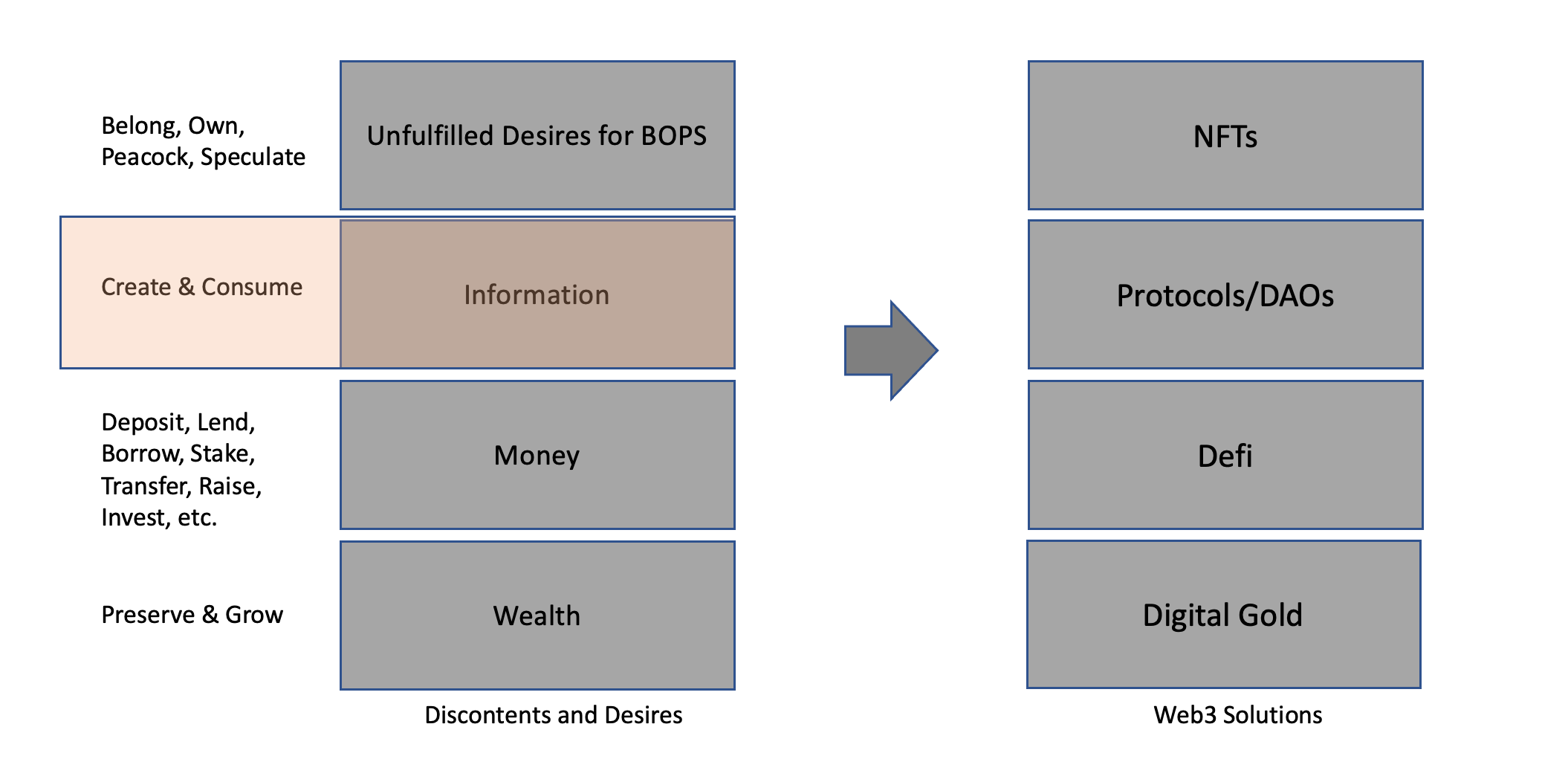

What is broken in our current models of information creation and consumption?

This is Part 2 of a series: Web3 and the Opposable Mind.

For context, this piece will specifically focus on the origins of our discontents in how we create and consume information in the internet age.

The internet’s primary “job-to-be-done” from the very beginning has been to facilitate information exchange among and between individuals and businesses. A super-brief history may help set some context.

Web1 (1990s-early 2000s) was peer-to-peer in its purest form. Anyone who wanted to publish could do so by running their own server. For most users, the web was read-only and the internet was filled with static pages and images— 99.9% of users consumed, 0.1% created. Neither identity nor payments was a part of internet protocols so every publisher created an identity system if they needed to.

Centralized aggregators/networks (early 2000s-2010) emerged to empower anyone to write to the web — any user could publish a profile, blog, or micro-blog without needing to be technical or set up a server. Identity was a core part of these networks.

Centralized infrastructure —like AWS—emerged starting 2005 to empower developers and fuel the SaaS revolution. It also made it easy to build new networks with web and mobile front-ends to connect supply and demand.

“Infrastructure as a service” enabled the creation of a whole bunch of new software-powered networks to hail a cab, rent a hotel, find a date, and more. Network here means cloud software running on a proprietary database that connects the demand-side of a market to the supply-side. A network offers different applications and value props for each side. Uber is the cab network. Airbnb is the BnB network. Google is an Information Network. Facebook is the social network. Tinder is the dating network.

We started calling this centralized stack—infrastructure + networks + SaaS apps— collectively as Web2 technologies (mid 2000s-now).

Web2 has been wildly successful and has billions of users; the mobile-cloud revolution has transformed the world and made information widely accessible. SaaS companies built on centralized infrastructure have helped millions of businesses become more productive and efficient.

New technologies replace the old only when they do a better job of solving the underlying user problem. New architectures mean little unless they can improve user economics or experience on at least one dimension that truly matters to them.

In several areas of Web2—like IaaS, PaaS, enterprise SaaS and consumer SaaS—there is good value alignment between the software company— its founders, investors, and employees,—and its 3rd party developers, customers, and users. There is little clamor to build Web3 alternatives to Salesforce CRM or Office 365 or Workday HR because they work well for the most part. [1]

The fault-lines come into sharper focus though for networks representing multi-sided marketplaces. To understand further, there is value to traversing back to the roots of the legal entity that underlies the modern company: The Joint Stock, Limited Liability Corporation.

The Origins of the Corporation

The corporation’s lineage goes back to ancient times. At a primitive level, it was about allowing people to organize around a shared mission, and create a legal and enforceable mechanism to do two key things: a) pull together money, brains, and brawn for specific purposes, and b) share risks and rewards commensurate to contributions and profits.

John Micklethwait and Adrian Woolridge provide a riveting example (slightly paraphrased below) in their short and breezy book, The Company: A Short History of a Revolutionary Idea.

“The Assyrians (2000-1800 BC) even had partnership agreements. Under the terms of one contract, some 14 investors put 26 pieces of gold into a fund run by a merchant called Amur Ishtar, who himself added 4. The fund was to last four years, and the merchant was to collect a third of the profits—terms not dissimilar to a modern venture-capital fund.”

There was the Muslim muqarada that was used to finance and manage voyages, the Italian Compagnia that was the earliest adopter of joint liability, and the Venetian and Florentian guilds that were granted monopolies of trade in specific markets.

The game-changing moment in the journey of the corporation though was the creation of state sponsored charter companies like the Dutch East India Company (called VOC in Dutch) and the British East India Company in the early 1600s. The extreme risks of voyages from the unknowns of sailing to the East Indies, the need to raise a capital pool to fund multiple voyages over a longer time horizon, and investors’ demands to buy or sell at any time led to two key innovations at scale: a) The idea of limited liability to limit investor exposure to the extent of their ownership, thereby protecting their personal assets, and b) The idea of capitalizing a company through shares and allowing for them to be traded in an exchange.

The joint stock, limited liability company was the fuel that powered the European colonization of the world for the next few centuries. At its peak, the British East India Company had a fighting force of 250,000 men and the Dutch VOC was once valued at an inflation adjusted value of $7.9 Trillion! (As an aside, William Dalrymple’s book, Anarchy, is a great read on how a private corporation ended up ruling 25% of the world and looted its colonies to enrich shareholders.)

You can draw a direct thru-line from the East India Companies of the 1600-1800s —sans the state sponsorship—to the modern Delaware Corporation. The Delaware Corp allow frictionless formation of companies in the modern era, and undergirds the entire startup, VC, and Big Tech ecosystem.

The idea of the company with its unbridled capitalistic ethos has been a resounding success. Innovations like Employee Stock Option Pools (ESOP) have expanded the benefits of stock ownership to key employees and have broadened the class of the wealthy, particularly in tech.

But focusing only on shareholders, founders, and top employees is increasingly problematic in a connected world with low transaction costs where community and ecosystem are the fundamental drivers of value creation. This is especially true for large tech intermediaries acting as networks.

Here are eight reasons at the heart of why the traditional company model is causing heartburn to users and non-owner stakeholders.

1. Decreasing Transaction Costs Increasing Misalignment

Ronald Coase wrote in 1937 in his seminal thesis, The Nature of the Firm, that transaction costs are the biggest reason for a firm’s existence. (Read Taylor Pearson for a more detailed drill-down on the topic.)

Transaction costs =

Triangulation costs (Cost to search and find the right supplier) +

Transfer costs (cost to negotiate, bargain, and pay) +

Trust costs (risks of non-delivery, low quality or late delivery, increased liability, etc.)

With low transaction costs, companies need few employees. They can orchestrate most of the work by engaging third parties on demand.

The internet enables this coordination at scale. Every day, tens of millions of riders find drivers, guests find hosts, and hungry consumers find dashers. None of them knew each other before the transaction, and most will never see the same person again.

Giant tech corporations like Uber, Google, Doordash, Amazon, Airbnb, etc. have aggregated both the long tail of fragmented suppliers and the billions of users who have come to rely on them. Their ecosystems (users, contractors, advertisers, etc.) are orders of magnitude bigger than their employees.

The incentive structures of the company though are still solving for shareholders first creating a misalignment of interests— both in terms of take-rates (revenue share) and ownership.

2. Inequitable Revenue Share /Take Rates

Big tech companies create significant value for users and advertisers. But as a natural extension of optimizing first for shareholders, the value captured (revenues) is not shared equitably with creators and other participants in the ecosystem.

Chris Dixon has an eloquent take on take rates.

and there are some good counter arguments too on if this is an accurate representation.

Hard to argue though that current take rates are reasonable. Ad-driven social networks (Twitter, FB, Google, etc.) take 100% of ad revenue. Transaction driven networks (Uber, Instacart, Doordash, etc.) take anywhere from 20-40%. Users and advertisers get no rewards beyond the core utility of the network and the occasional credit or coupon.

3. Inequity in Ownership

Majority of corporate shares of tech intermediaries are held by investors, founders, and executives. The early users and customers who took risks on the company, the marketplace supply cogs (a la drivers, dashers, contractors, etc.) who provide liquidity, etc. rarely have any meaningful ownership. Users’ time, money, data, and attention, and network participants’ contributions drive value creation. But the relative payoff for shareholders is multiple orders of magnitude higher creating resentment.

4. Shareholder-First Ethos

The goal of optimizing first for shareholders has meant that posturing notwithstanding, management teams and boards have no incentives to bother with anything other than solving for growth and valuation. Anyone not a shareholder, and anything not in the direct line of these goals becomes secondary.

5.Opaque Governance

Boards are dominated by the marquee investor class. Governance is mostly opaque, notwithstanding transparency theater. Archaic SEC rules and legalese erect formidable barriers for participation from small shareholders or the broader community.

This also extends to policy level decisions. Black-box algorithms decide which content is boosted or suppressed. Users do not have adequate choice on how their feeds should be sorted and what they want to see. The community lacks a formal voice in shaping policy.

6. Censorship

Powerful companies with trillions in market cap and billions of users can censor creator content, close developer APIs, and de-platform those who do not comply with arbitrary standards.

7.User Lock-In and Lack of Portability

Users’ personal data (social graphs, shopping data, billing data, policy data, etc.) are not portable across services. The extractive model limits exit options and restricts competition.

As Albert Wenger says here,

the fundamental source of monopoly power in the digital world is network effects arising from the control of data….This will continue to lead to power law size distributions in which the number 1 in a market has a dominant position and is many times bigger than the number 2…. The only way to go up against this effect is to shift computational power to the network participants.

8. Data Leakage and Lack of Privacy

Users’ entrust their personal data to a wide range of suppliers—Utilities, Telcos, Banks, Retailers, etc.—but data leakage is all too common. Rich repositories of user data are honeypots that attract hackers. Data brokering companies and Ad-tech vendors actively trade in the buying and selling of personal data.

These discontents are all too real for creators, contractors, developers, and users. The wide gaps between those above the API and those below the API and the dependence on these platforms for their livelihoods reinforce a new reality: we need either effective anti-trust action and regulation (or) a viable new alternative. Is regulation and reform feasible [2] and can it be effective? Or is long-term disruption more likely to come from left-field alternatives that are re-imagining the economic contract between a platform and its users, third party developers, content providers, and investors?

[1] There are indeed several areas of discontents among SaaS users—like supporting more flexible identity and payments, stronger privacy, data portability, etc.—but they assume less importance relative to functional and UX considerations.

[2] US anti-trust statutes are more than 100 years old. They never imagined demand aggregators —like Facebook, Google, or Amazon—who might deliver substantial consumer benefits but still do long-term harm to consumers by increasing lock-in. Half-baked regulations can have unintended effects of strengthening the incumbents while making it harder for new start-up alternatives to be in compliance, get exits, or raise capital.